M&A Insurance: Quarterly Market Update – Q4 2024

Strong finish to 2024

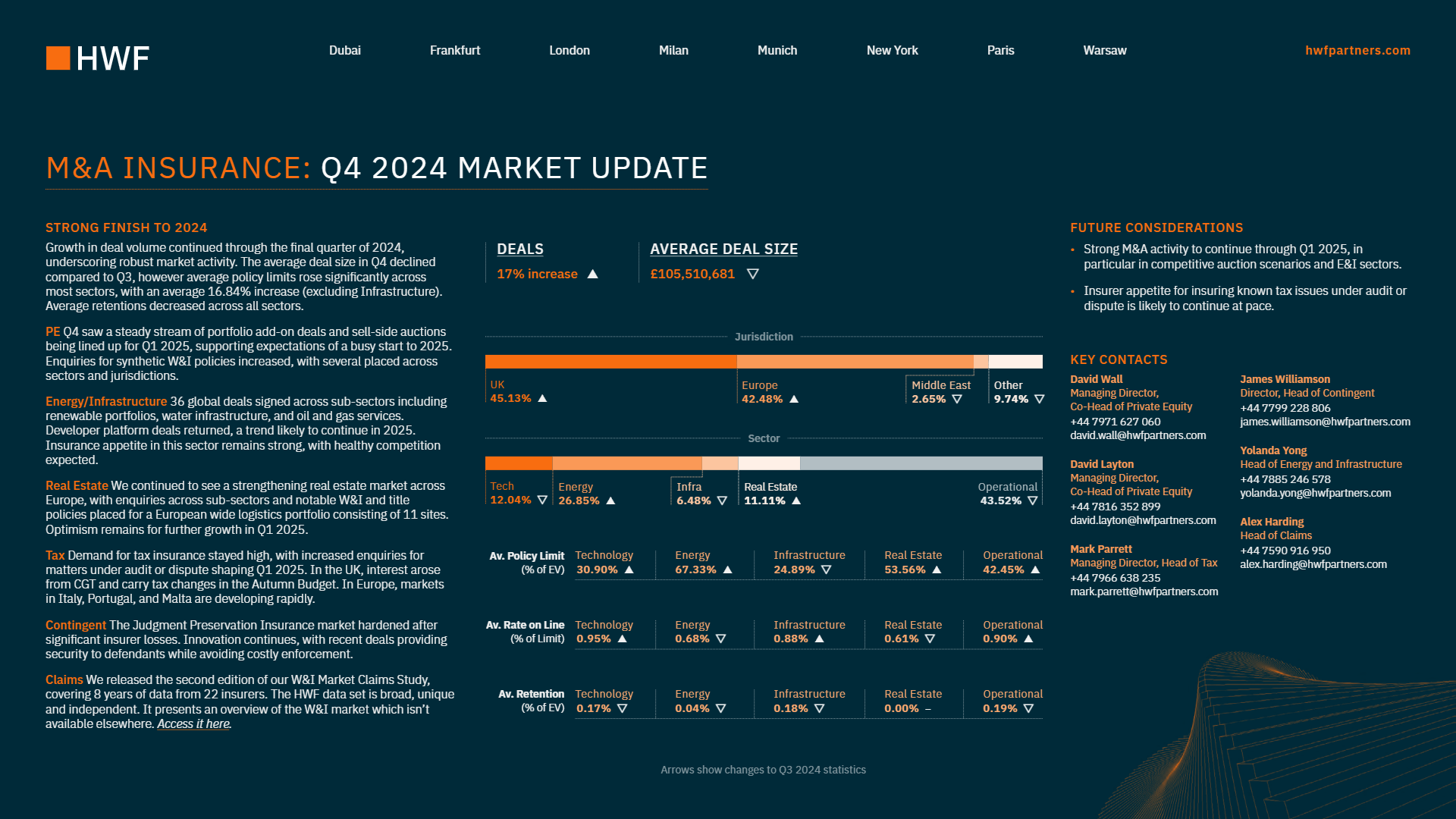

Growth in deal volume continued through the final quarter of 2024, underscoring robust market activity. The average deal size in Q4 declined compared to Q3, however average policy limits rose significantly across most sectors, with an average 16.84% increase (excluding Infrastructure). Average retentions decreased across all sectors.

PE: Q4 saw a steady stream of portfolio add-on deals and sell-side auctions being lined up for Q1 2025, supporting expectations of a busy start to 2025. Enquiries for synthetic W&I policies increased, with several placed across sectors and jurisdictions.

Energy / Infrastructure: 36 global deals signed across sub-sectors including renewable portfolios, water infrastructure, and oil and gas services. Developer platform deals returned, a trend likely to continue in 2025. Insurance appetite in this sector remains strong, with healthy competition expected.

Real estate: We continued to see a strengthening real estate market across Europe, with enquiries across sub-sectors and notable W&I and title policies placed for a European wide logistics portfolio consisting of 11 sites. Optimism remains for further growth in Q1 2025.

Tax: Demand for tax insurance stayed high, with increased enquiries for matters under audit or dispute shaping Q1 2025. In the UK, interest arose from CGT and carry tax changes in the Autumn Budget. In Europe, markets in Italy, Portugal, and Malta are developing rapidly.

Contingent: The Judgment Preservation Insurance market hardened after significant insurer losses. Innovation continues, with recent deals providing security to defendants while avoiding costly enforcement.

Claims: We released the second edition of our W&I Market Claims Study, covering 8 years of data from 22 insurers. The HWF data set is broad, unique and independent. It presents an overview of the W&I market which isn’t available elsewhere. Access it here.

Future considerations

Strong M&A activity to continue through Q1 2025, in particular in competitive auction scenarios and E&I sectors.

Insurer appetite for insuring known tax issues under audit or dispute is likely to continue at pace.