M&A Insurance: Quarterly Market Update – Q3 2024

Deal volumes surge

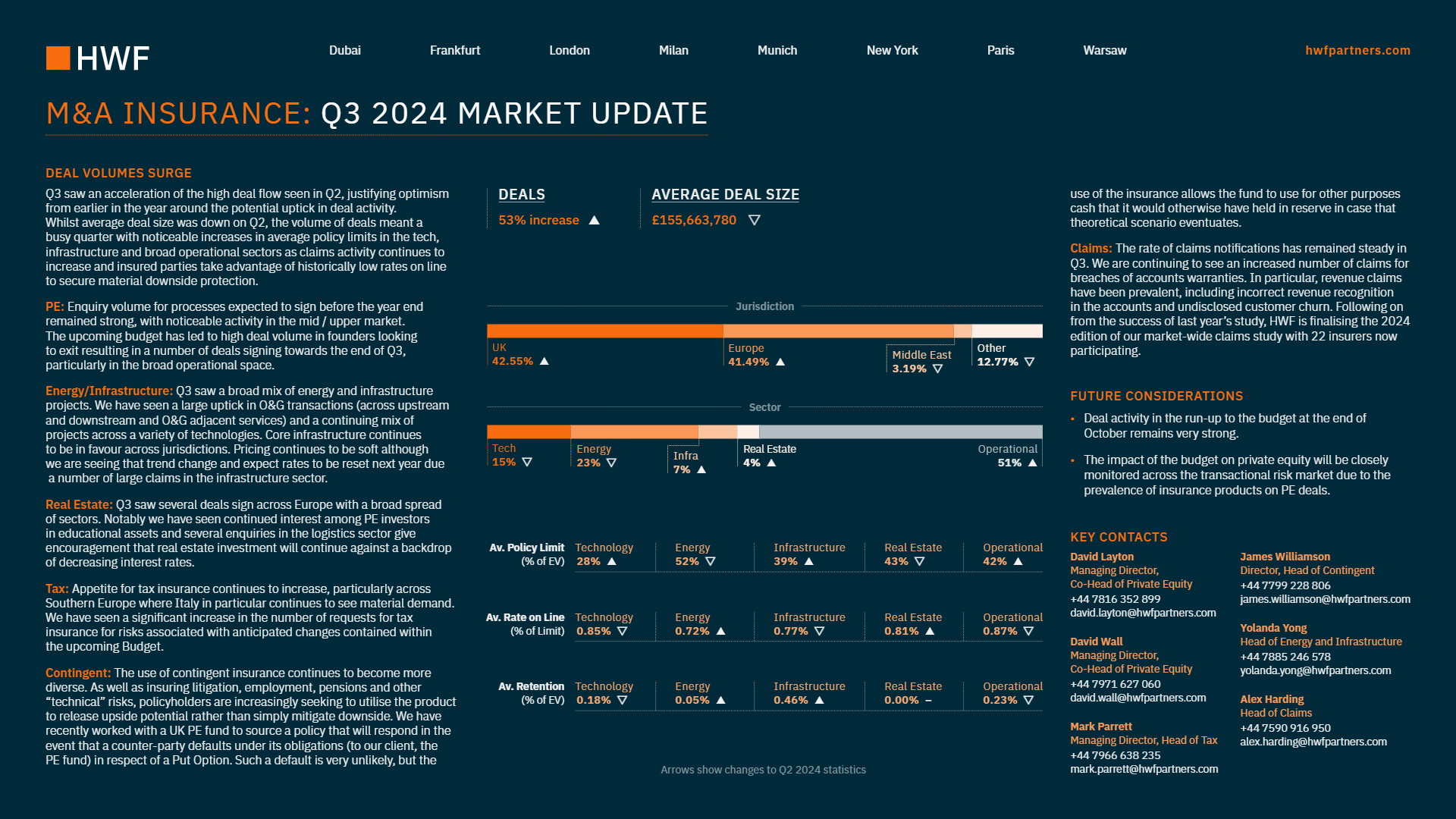

Q3 saw an acceleration of the high deal flow seen in Q2, justifying optimism from earlier in the year around the potential uptick in deal activity. Whilst average deal size was down on Q2, the volume of deals meant a busy quarter with noticeable increases in average policy limits in the tech, infrastructure and broad operational sectors as claims activity continues to increase and insured parties take advantage of historically low rates on line to secure material downside protection.

PE: Enquiry volume for processes expected to sign before the year end remained strong, with noticeable activity in the mid / upper market. The upcoming budget has led to high deal volume in founders looking to exit resulting in a number of deals signing towards the end of Q3, particularly in the broad operational space.

Energy / Infrastructure: Q3 saw a broad mix of energy and infrastructure projects. We have seen a large uptick in O&G transactions (across upstream and downstream and O&G adjacent services) and a continuing mix of projects across a variety of technologies. Core infrastructure continues to be in favour across jurisdictions. Pricing continues to be soft although we are seeing that trend change and expect rates to be reset next year due a number of large claims in the infrastructure sector.

Real estate: Q3 saw several deals sign across Europe with a broad spread of sectors. Notably we have seen continued interest among PE investors in educational assets and several enquiries in the logistics sector give encouragement that real estate investment will continue against a backdrop of decreasing interest rates.

Tax: Appetite for tax insurance continues to increase, particularly across Southern Europe where Italy in particular continues to see material demand. We have seen a significant increase in the number of requests for tax insurance for risks associated with anticipated changes contained within the upcoming Budget.

Contingent: The use of contingent insurance continues to become more diverse. As well as insuring litigation, employment, pensions and other “technical” risks, policyholders are increasingly seeking to utilise the product to release upside potential rather than simply mitigate downside. We have recently worked with a UK PE fund to source a policy that will respond in the event that a counter-party defaults under its obligations (to our client, the PE fund) in respect of a Put Option. Such a default is very unlikely, but the use of the insurance allows the fund to use for other purposes cash that it would otherwise have held in reserve in case that theoretical scenario eventuates.

Claims: The rate of claims notifications has remained steady in Q3. We are continuing to see an increased number of claims for breaches of accounts warranties. In particular, revenue claims have been prevalent, including incorrect revenue recognition in the accounts and undisclosed customer churn. Following on from the success of last year’s study, HWF is finalising the 2024 edition of our market-wide claims study with 22 insurers now participating.

Future considerations

Deal activity in the run-up to the budget at the end of October remains very strong.

The impact of the budget on private equity will be closely monitored across the transactional risk market due to the prevalence of insurance products on PE deals.